Loan approvals used to be perceived as one of the daunting tasks for people. But in today’s digital-first landscape, loan approvals now happen in minutes, which implies that Non-Banking Financial Companies’ (NBFCs) online reputation is no longer completely built on interest rates; it is majorly built on transparency, trust, and a digital feedback loop. How you’re managing your lending app’s online reviews determines how many consumers will trust its offerings. That’s why you need online review management for NBFCs and lending apps.

According to 2024, The Financial Brand’s study has revealed that 90% of banking consumers are more likely to use online reviews to make informed banking decisions, including taking loans. So even a 1-star rating on your NBFC or lending app can majorly impact its online reputation, customer confidence, and loan disbursement volumes.

If you own an NBFC or lending app, let us tell you that reviews are not just vanity metrics. You must consider your online reviews critical early warning systems for technical glitches, operational inefficiencies, and customer satisfaction.

In today’s crowded market, how you respond and manage online reviews reflects your lending app’s longevity. This blog will explore how NBFC and lending app owners can effectively transform feedback into a powerful tool for building credibility, acquiring new users, and ensuring compliance for your lending apps. Let’s get started with an effective review management guide for your NBFCs and lending apps.

What Is Review Management for NBFCs and Lending Apps?

It refers to the strategic process of generating, responding to, analyzing, and monitoring user feedback across multiple platforms, including the Google Play Store, App Store, and social media. Advanced review management for lenders goes beyond just reputation management—it helps them identify potential technical issues in their apps, manage borrower grievances, and comply with regulatory guidelines.

Apart from this, review management helps NBFCs and lending apps build customer trust in a high-security industry like NBFCs and lending.

Customer review management for NBFCs and lending apps is a time-consuming process, as successful review generation and responding takes a significant amount of time.

So, if you desire to witness an overnight outcome of your strategy plan, a thorough review of the management strategy plan may not help you. It requires time to get the desired results. Now that you have a clear idea of what review management actually is for NBFCs and lending apps, let’s talk about how it can benefit your loan app business as well.

Why NBFCs and Lending Apps Must Prioritize Effective Review Management?

Managing app reviews on loan apps is critical for NBFCs and lending app owners. Why? Mostly because their business models heavily depend on digital trust and speed.

When you effectively manage the reviews for your NBFCs, it helps you acquire new customers and brand equity. From establishing customer trust and influencing loan acquisition decisions, strategic review management comes with an extensive list of advantages. Let’s have a look at the list of the top 6 key benefits:

- Builds Customer Trust

Your prospective app users mostly trust peer reviews just as they do personal recommendations. You must be wondering why!

When real users who have already used these NBFCs and other lending apps share a high volume of reviews and thoughtful responses for your app, it signals that the lender is transparent, legitimate, and cares about its customers. Such lending apps often face scepticism because of their relationship with financial services. An effective review management strategy requires you to respond to negative feedback that convinces other potential clients that your company values its clients’ opinions.

- Influences Loan Application Decisions

A high star rating on your NBFC app can directly correlate with download probability. Do you know that high-rated apps attract up to 3x more downloads than the lower-rated ones?

A high review volume shows that you have a good number of loyal app users. It will significantly influence the loan application decisions, as when you generate detailed reviews and prompt responses, it will help the potential users assess the speed, fairness of the app, and the interest rates. It will eventually reduce their anxiety regarding sharing sensitive KYC information.

- Impacts App Store Rankings

Review management for NBFC apps majorly impacts your lending app store rankings on Google Play Store and Apple App Store. A higher rating and a high volume of recent reviews for the app can improve its visibility across the app store and the local search results as well. It will help lenders get found in a crowded financial industry.

Google Play Store and Apple App Store algorithms majorly prioritize ratings and reviews. They mostly favour fresh content and recent reviews of their apps. Effective review management helps your lending app rank higher on app stores and indicates that the app is functional, updated, and reliable as well.

- Improves Online Visibility

Customer review signals specifically contribute to the local SEO rankings of your NBFCs and lending apps. It helps you rank your app in Google Map Packs. Effective review management requires you to generate more positive reviews that will act as user-generated content. It provides fresh and relevant keywords that help NBFC sites and apps rank higher in organic online searches.

- Protects Brand Reputation

Negative reviews are inevitable; even a single negative review can destroy your years of effort to build a strong online reputation. Effective review management requires you to deal with negative reviews and complaints. When you respond professionally and calmly, even to a negative review, it can turn a dissatisfied customer into a loyal advocate and prevent long-term damage.

Online review management for NBFCs can help you professionally respond to negative reviews and protect your app’s online reputation. In today’s highly competitive digital landscape, well-managed reviews can help prevent fake or malicious negative feedback from dominating the search results as well as the brand perception.

- Helps Detect Operational Issues

Do you know that online reviews serve as a real-time, zero-cost review mechanism? Otherwise, it will be difficult for you to identify your app’s area for improvement. When your existing app users share their experience through reviews, the reviews highlight specific bugs, app crashes, and flaws in the user journey that you can convey to the developers, and they can fix them to improve the app’s performance.

Such issues, such as customer support delays and unexpected fees, are often mentioned in the reviews. They allow leadership to identify and rectify internal procedural problems of your app and significantly improve its overall service quality.

5 Key Platforms Where Reviews for NBFCs and Lending Apps Appear

Online reviews for non-banking financial companies and digital lending apps are quite crucial for users as they make informed financial decisions through the apps. The users can often assess reliability, interest rates, and customer service.

Effective review management strategies for financial services require NBFCs and lending app owners to focus on some crucial platforms where mostly the reviews appear. Targeting such platforms can help you get access to a large volume of reviews and valuable insights into your app user feedback.

Here are some key platforms where NBFC and lending app reviews commonly appear. Let’s have a look:

- Google Play Store

This is the primary source for most Android app downloads; almost a thousand Android apps have surpassed the one-million download milestone. This specific play store is critical for real-time user experiences, customer service feedback, and app performance issues.

When you focus on making your lending app rank higher across the Google Play Store, it naturally grabs the attention of your target audience and helps you acquire new users for your lending app.

- Apple Play Store

Users of iOS devices use the Apple App Store to rate and review lending apps. Targeting the Apple App Store can help you attract iOS device users and attract new downloads.

Reviews on Apple Play Store often focus on user interface, usability, and app functionality. Reviews for NBFCs and lending apps often appear on the Apple Play Store, giving the clarity of the apps’ credibility and reliability to the potential app downloaders.

- Google Reviews

Just like the Google Play Store reviews, Google Business profile Reviews are essential for NBFCs and Lending app owners.

Google Business Profile reviews, or Google reviews, are used to offer insights into customer satisfaction with loan collections and servicing. When someone searches for a lending app on Google, the reviews appear on the first page of search results.

- Trustpilot

This is one of the most popular open-to-all review platforms where most consumers build trust with businesses. Trustpilot has firmly positioned itself as a primary hub where anyone can write about any sort of business. It receives more than 4 million new regional online channels every month, which is quite difficult to compete with. Users mostly consider the legitimacy of lending platforms, and people often share detailed feedback on the overall customer experience.

Trustpilot mainly focuses on hosting reviews for B2C companies, just like the other review sites, such as Amazon Customer Reviews, TripAdvisor, and Yelp. Targeting Trustpilot can help you grab the attention of the right customer base and acquire new clients for your NFBCs and lending app.

- Social Media and Fintech Forums

Platforms like Reddit and other specialized finance forums are key places where transparent and mostly anonymous discussions regarding P2P lending platforms, default rates, and app reliability take place. The borrowers mostly share authentic feedback on social media platforms like Facebook and X, including airing grievances against lending apps.

- Did you Know?

If your NBFCs and lending app don’t have an official brand presence on the Play Store and have combined negative reviews on social media regarding data security. It often indicates the existence of illegitimate or fraudulent lending apps across the Play Store.

5 Common Review Management Challenges Faced by NBFCs and Lending Apps

Just like benefits, effective online review management for NBFCs and lending apps comes with certain challenges as well. If you fail to identify the challenges, you cannot prevent the long-term damage of the reputational risks.

Overlooked challenges can severely impact customer acquisition and trust. As financial services have a sensitive nature, the following challenges can actually ruin your years of efforts to build a strong and positive review base.

Below are some common challenges you can face while managing reviews for your NBFCs and lending apps across the web and the Play Store. Let’s have a look:

- Fake or Misleading Reviews

Your market competitors and malicious reviewers can often target your lending apps, and NBFCs specifically sabotage your reputation. On the other hand, some fraudulent lending apps may use fake, overly positive, or unreal reviews to manipulate users.

These types of reviews can distort the genuine customer experience and make it difficult for users to trust the platform. It can lead to misleading reports on app stores or rating platforms as well.

- Negative Reviews from Rejected Applicants

If you own an NBFC and a lending app, you may receive a significant portion of reviews from your users whose loan applications were rejected mostly because of poor credit scores, incomplete documentation, and insufficient income. In such situations, the rejected applicants are more likely to express their frustration through emotional and low-star ratings.

Such reviews often don’t reflect the service quality, but rather show the disappointment of the rejection, which can result in extreme damage to the online reputation of the lending app owners.

- Loan Rejection Frustrations

App users often complain about a lack of transparency regarding why their loan application was rejected. It leads to many public perceptions of unfair treatment from your company’s end. If a lender doesn’t provide a clear ‘adverse action notice’ to the potential users regarding why they reject the loan application, it will definitely invite backlash.

Increased public complaints related to ‘sudden’ or ‘unjust’ rejections can damage your lending app business’s image and may create a negative public perception that the app is not at all reliable.

- Complaints about Recovery Practices

We all know that online reviews related to your NBFCs and lending apps often highlight aggressive or unethical recovery practices. As per RBI guidelines, recovery agents are restricted in their communication methods – so the complaints regarding harassment, calls to relatives, and unethical calling times persist.

Such reviews are highly damaging to the reputation of your NBFCs and lending app, resulting in legal scrutiny, regulatory penalties, and significant loss of consumer trust.

- Data Privacy Concerns

Digital lending apps generally require extensive permissions to evaluate creditworthiness. The users frequently leave negative reviews where they voice their customer concerns about how their data is used, stored, and misused.

Fear of data theft or blackmail causes high-risk ratings, while, on the other hand, complaints regarding this specific reason can trigger cybercrime investigations and regulatory action against the lending app.

An Ultimate Review Management Guide: 6 Must-Know Strategies for NBFCs and Lending Apps

Digital presence is the primary business channel for the non-banking financial companies and lending apps. Effective online review management for NBFCs and lending apps is one of the crucial parts of the ultimate process of building a strong online reputation.

Wondering how you can build and manage your lending app business’s online reputation through effective review management?

Don’t worry! We have come up with a comprehensive review management guide that you can strictly follow to boost your digital reputation for your review management. In the guide, we have enlisted the top 6 review management strategies that you must implement. Let’s have a look:

Strategy 1: Monitor Reviews across All Platforms

While monitoring the reviews you have received for your NBFCs and lending apps across the web, you must prioritize all the platforms where your app review may appear. If you ignore any of the platform’s features, you may not be able to target the right audience, which will not be extremely fruitful for your business.

Here are two primary ways to effectively monitor reviews across all the platforms:

- Use Reputation Monitoring Tools

Relying on manual checks is completely insufficient for NBFCs and lending app owners. Advanced online reputation management software can help you enable 24/7 manual monitoring across hundreds of platforms.

Online reputation management services often involve the right implications of these tools.

Once you have a clear idea of the review management strategies, the right implementation of the tools can help you make the process seamless and guarantee your desired results. Tools like Brand24, Reputation.com, Google Alerts, and more can help you simplify the entire process of effective review management for your NBFCs and lending apps. We will talk about the variety of tools later in this blog.

Why choose tools? Tools consolidate reviews, social media mentions of your lending apps, and surveys into one AI-powered centralised dashboard. The review generation that takes more than a week can be completed within just a few hours with the effective implementation of review monitoring tools.

You can compare the review monitoring and sentiment analysis tools that help you identify a noticeable increase in negative sentiment before the reputational risk escalates.

- Track Ratings Regularly

Online review monitoring for lending apps requires you to track their ratings regularly. The rating of different lending apps can change over time.

What are app ratings? These are some direct indicators of user trust and influence on app store rankings. A sudden drop or increase in your app store ratings can help you identify the problems or improvements in your lending app.

You can use tools like ReviewPush or BrightLocal to monitor the app ratings across the major app stores. For this, you need to analyze the recurring keywords in low ratings to identify technical bottlenecks.

Strategy 2: Generate Positive Reviews from Your Satisfied Customers

Now the second step is to generate positive reviews from your customers who are satisfied with your app services. You need to ask for the review even if the customer is satisfied with your lending app services.

Do you know that even your satisfied customers will not share a review if you don’t request or encourage them to?

It requires you to ask for the reviews at the correct time and in the right way. Let’s have a look at how you can successfully generate reviews from your app users:

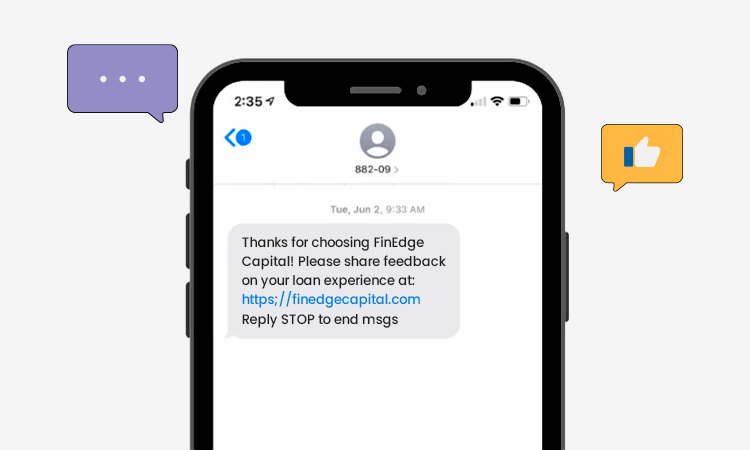

- Ask for Reviews Promptly

The first and foremost thing you need to do is to reduce the effort which is required for an app user to leave a review. You can do it by providing a direct and one-click destination.

Firstly, you need to create a ‘get more reviews’ link in the Google Business Profile and share the link directly via WhatsApp, email, or SMS.

Time plays a huge role here. If you send automated review requests to your users after a week, it will make no sense to them, and they may ignore them. You need to send the request at least within 1-2 days after someone downloads the app.

- Share QR Codes and Links to Your Review Page

You need to share the QR codes and links to your review page through the Google Business Profile. Sharing the review link or QR codes through WhatsApp, email, and SMS can help you make the review submission process easier for the users.

You can share it directly through WhatsApp, Email, and SMS. It will make the review submission process easier for the users – they will know exactly where to share the reviews.

You need to display the QR codes at the front desk of your office, on the desk of your loan officers, and on loan documentation for in-person customers. You can use in-app SDKs that allow users to rate the app, and for this, they don’t need to leave the app’s interface. It will eventually increase the response rates.

- Make the Review Submission Process Seamless

If your app users need to jump through hoops and go through many steps to submit one review, you may need to integrate review requests into your loan management system.

So, the process should be like this – when a loan status moves to ‘Disbursed’, an automated trigger sends a follow-up message to the app user. You need to use in-app review prompts to generate reviews rather than forcing the app users to open an external browser or store page. This trick will make the review generation process more seamless.

- Send Post-loan Feedback Emails

Email is a powerful channel when it comes to gathering detailed and high-quality reviews from your NBFCs and lending apps. A study has revealed that 61% of people prefer for brands to contact them through email.

Sending a post-loan feedback email is one of the best ways of online review management for NBFCs and lending apps.

What you need to ensure: You need to send the email 2-3 days after the disbursement to allow the app user to experience the service. However, try to contact them when the satisfied feeling is still fresh in the minds of your app users.

- The Structure to Follow for the Post-Loan Feedback Emails:

Subject: How was your experience, (name of the app user)?

Content: You must acknowledge the recent loan and thank them for downloading their app. Don’t forget to explain why their feedback helps others to choose the right app for their lending requirements.

Call to Action: Add a large, direct call to action button saying ‘Leave a Review Here’.

Personalisation: You need to address the app users by their name and reference their specific interaction.

Strategy 3: Respond to Reviews

Responding to reviews for NBFCs and lending apps is critical to build user trust, maintain regulatory compliance, and manage online reputation for their lending business. NBFC app owners must follow a proactive, empathetic, and professional approach that turns criticism into new app improvement opportunities.

You cannot just respond to online reviews with a normal reply.

For example, a little ‘thank you’ may not work for your satisfied app users, while on the other hand, a ‘sorry ‘ cannot fix an issue with users who have submitted a negative review.

- Respond Quickly to Complaints

You need to monitor the app stores like Google Play and Apple App Store, along with social media. Try to respond to a review within the first 24-48 hours after the app is downloaded. It will show that your business values user concerns and opinions the most. If any of the reviews report a bug, you must respond to confirm investigation and follow up once the issue is resolved.

It’s quite common for your lending business to receive negative reviews, as this is related to financial services. You must promptly respond to the complaints and try to resolve the issues through your responses.

- Show Your Empathy and Offer Solutions

You need to acknowledge the user’s emotional state, especially the frustration over loan rejections or high interest rates. Even for the negative reviews, you need to maintain the utmost empathy and professionalism while responding to them.

If the reviewer is angry or disappointed, it can reduce the anger and showcase professionalism from your end. You should never blame the user for experiencing an inconvenience with your lending app.

- Handle Negative Reviews Effectively

Handling negative reviews can help you sort out issues with those app users who don’t have positive experiences with your NBFCs and lending apps.

Stop being defensive and never consider deleting the complaints. We suggest you not get involved in a public argument; you can take the conversation offline if you think that it can escalate and cause major reputational issues.

Here, the strategy is to treat the negative reviews as free and high-value consulting that highlights specific and actionable problems. When your users get the desired solution they need, it will definitely turn a criticism into an opportunity to regain their trust.

- Example Response Framework for Negative Reviews

Here is a robust framework for how you deal with negative reviews:

- Stay Professional – You must stay professional while responding to positive, negative, or neutral reviews. The response should be professional enough to showcase that you value your users’ opinions and try to provide a perfect resolution for the inconvenience caused.

- Acknowledge the Issue – Secondly, you need to acknowledge the issue conveyed through a negative review. When you respond, you must highlight the issue to showcase that you have thoroughly read the reviews

- Apologise if Necessary – We sincerely apologise for the inconvenience and frustration that the lending app caused the user.

- Take the Conversation Offline – You should take the conversation offline if things are not working right. It’s better not to encourage an argument online, as it can even escalate the situation and make it even worse.

- Investigate the Complaint – You can ask to take some time to properly investigate a situation and then offer a suitable resolution.

- Provide Resolution—”We want to make things right!”—you need to convey it through the review response.

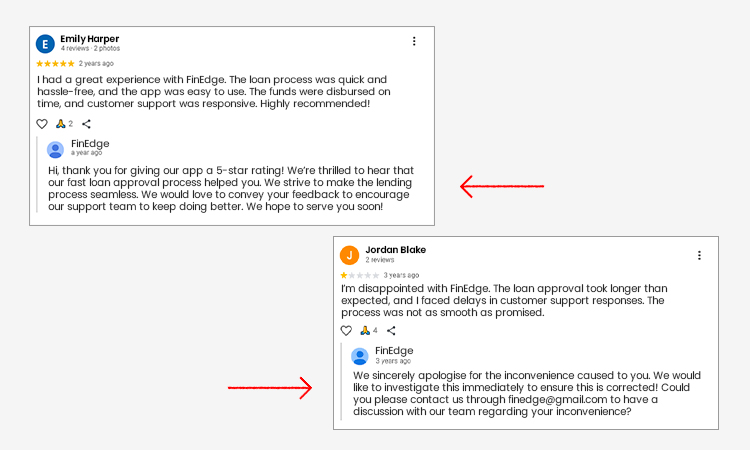

- Sample Example of Response to Positive Reviews

“Hi, thank you for giving our app a 5-star rating! We’re thrilled to hear that our fast loan approval process helped you. We strive to make the lending process seamless. We would love to convey your feedback to encourage our support team to keep doing better. We hope to serve you soon!”

- Sample Example of Response to Negative Reviews

“Hey (reviewer’s name), we sincerely apologise for the inconvenience caused to you with our NFBC’s repayment feature. This is not the standard we set for ourselves! We would like to investigate this immediately to ensure this is corrected! Could you please contact us through (your official email ID) to have a discussion with our team regarding your inconvenience?”

- Sample Example of Response to Neutral Reviews

“Hey (reviewer’s name), thank you for taking the time to share your feedback. Our team is glad to know you found our interest rates competitive. We’re sorry to hear about the difficulty you faced with the document uploads in our app. We are rigorously working on improving the app’s document-scanning tool. At (your company name), we appreciate your insights to help us get better.”

Strategy 4: Quickly Resolve Customer Issues

As part of your online review management for NBFCs, you need to offer prompt resolutions for customer issues.

You must provide frontline agents with the authority to resolve the common service issues immediately. However, this should not require multiple layers of management approval from your company’s end.

Apart from this, you must know how to implement AI-powered chatbots, in-app messaging, 24/7 exceptional support for initial inquiries, and WhatsApp bots for basic complaint registration. You must establish a strict service level agreement for acknowledging complaints immediately and resolving them within 3-5 business days.

We suggest offering consistent support across channels, including apps, email, social media, and phone. It must centralize the data into a CRM system to ensure no complaint is overlooked from your end.

- How to simplify complaint registration for app users?

It’s important to make the complaint registration process seamless. You need to make it easy for the app users to directly lodge complaints on the mobile app. For this, you need to provide a tracking number or a docket number to monitor the status of their grievances.

- Prioritise Grievance Redressal to Reduce Negative Reviews

Always prioritize responding to the negative reviews on public forums like App Store, Play Store, and social media sites within 24 hours. No matter how much criticism the review contains, you must address it with empathy and direct it to private online digital channels for suitable resolutions.

A Pro Tip! When you handle a negative review well and resolve the issue, the user is more likely to share their positive experience, and can improve the overall app ratings.

Strategy 5: Maintain Transparency throughout the Process

It’s one of the most crucial parts of effective review management for your NBFCs and lending apps. Now the question comes – how can you maintain transparency?

You need to provide the following information to the users –

- All-inclusive cost breakdown

- Standardised loan agreements

- No hidden fee policies

- Interest rates

- Processing fee details

- Repayment terms

- Loan repayment schedule and the implications of late payments

- Standardized agreements

- Grievance redressal transparency

You must ensure that all the charges are completely disclosed through the RBI-mandated fact sheets. Try to provide the details in the regional language for better understanding.

Strategy 6: Leverage Positive Reviews for Brand Growth

Review generation is not the only thing you need to do to manage your NBFC’s online reputation. You must know how to leverage the positive reviews you’ve generated.

As trust is the primary currency for your lending app users, you must showcase user-generated content, such as positive testimonials, where users can showcase how they’ve benefited from your lending app.

Why? Positive feedback serves as social proof, and it reduces the potential app user’s anxiety and accelerates the conversion rates by a huge margin.

- Showcase your Positive Testimonials

Here we will talk about how you can showcase your positive user testimonials in the most effective way:

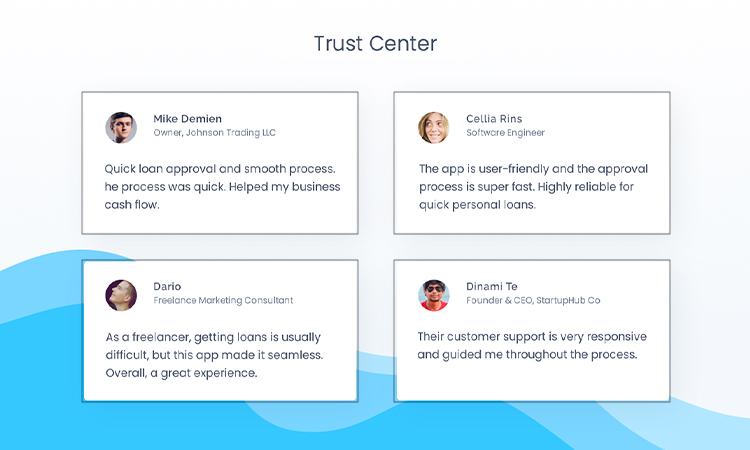

- Dedicate a page: You need to dedicate a section of your website, such as a ‘Trust Center’ page, where you will feature headshots of your app users, their names, and specific quoted feedback. However, you need to take permission from the users before using their photos and other details for your promotional purposes.

- Use carousels: You must implement a review carousel on the homepage of your site. Apart from the homepage, you can also implement the carousel on the loan application and checkout pages to provide immediate reassurance.

- Use Reviews in Marketing Campaigns

Now it’s time to use the reviews in a variety of marketing campaigns:

- You can turn a 5-star review into engaging visuals for Instagram, LinkedIn, and Facebook. You can tag the reviewers as well to increase your page reach.

- You can include short customer quotes in your Google Ads and Facebook Ads. It will help you increase the click-through rates and reduce ad costs through higher relevance.

- For the email campaigns, you can feature ‘top-rated customer stories’ to encourage more app downloads.

Common Tools for Review Management for NBFCs and Lending Apps

Now that you already have an idea about how you can strategise your plan to effectively manage the reviews for NBFCs and lending apps, it’s time to know about some tools that can help you simplify the process of effective review management.

Here are the top 5 types of review management tools that you must employ to manage your reviews for NBFCs and lending apps. Let’s have a look:

- Review Monitoring Platforms

The following are the top 5 review monitoring platforms that NBFCs and lending app owners can employ to effectively manage customer reviews. Explore the list and choose what suits your specific requirements:

| Review Monitoring Tool Name | Features to Use |

| 1. Exotel | • Provides cloud telephony-driven solutions • Provides automated SMS/voice-based review requests |

| 2 Birdeye | • AI-powered review management platform • Helps monitor more than 200 sites and generate reviews • Provides AI-based responses to reviews |

| 3. Clappia | • No-code, AI-powered platform that allows for the rapid creation of customized apps • Can build apps for inspections, audit, and field agent monitoring • Enables tracking of agents and geo-tagging of locations, ideal for multi location businesses |

| 4. GoCollect App | • Provides real-time tracking features for on-field agents and digital payments • Ideal automated debt collection mobile app designed for on-field teams • Uses AI to identify the best time, date, and location to contact a borrower |

| 5. Credgenics | • Comprehensive SaaS-based platform for end-to-end loan collections and debt resolution for banks, NBFCs, and fintechs • End-to-end digital-first, data-driven, and secure technology solution • Uses AI-driven voicebots and omni-channel communication |

- Sentiment Analysis Tools

Here are some popular sentiment analysis tools you can choose from to boost your review management efforts for your NBFCs and lending apps:

| Sentiment Analysis Tools | Features to Use |

| 1. Clooktrack | • Focuses on surfacing consumer themes, sentiment trends, and emerging issues across channels |

| 2. Sentisum | • Used for analyzing support tickets and feedback to uncover actionable insights |

| 3. Enterpret | • Specializes in analyzing text-heavy feedback to map it to specific customer themes |

| 4. Medallia | • A top-tier text review analytics tool that analyzes sentiment across social media, surveys, call transcripts, and app reviews |

| 5. Brand24 | • Tracks review and brand mentions in real-time across social media and the entire web • Provides AI-driven sentiment analysis and alerts • Helps to tune sentiment models for finance-specific slang |

- Social Listening Tools

Social listening plays a huge role in online review management for NBFCs and lending apps. From detecting crises before they grow and identifying both in-app complaints and broader online sentiment:

| Social Listening Tools | Features to Use |

| 1. Talkwalker | • Monitors online reviews, surveys, and social media in real-time |

| 2. Meltwater | • AI-powered sentiment analysis and tracking brands across social media, news, podcasts, and video |

| 3. Sprout Social | • All-in-one social management platform • Ideal for robust listening and automatic tagging of sentiment for incoming messages |

| 4. YouScan | • Specializes in visual listening across TikTok, Instagram, and other social media platforms |

| 5. MarketBeam | • Focuses on amplifying positive brand mentions |

| 6. Quickmetrix | • Indian-based tool popular for financial services • AI-powered sentiment and trend analysis for BFSI |

- CRM-based Feedback Systems

Here are some CRM-based feedback systems that NBFCs and lending app owners use to manage their online reviews. You can choose among the tools that you can directly integrate customer feedback into CRM systems for a unified view of the customer:

| CRM-based Feedback Systems | Features to Use |

| 1. Salesforce Financial Services Cloud | • Provides a 360-degree view of the customer • Allows integration of feedback and support logs |

| 2. SimpleCRM | • A customizable CRM solution that is popular for tracking customer interactions and feedback, including SMS/WhatsApp integration |

| 3. TeleCRM | • Helps in tracking call-based feedback and allows agents to directly log sentiment from customer conversations |

| 4. Roopya | • Ideal B2B fintech platform used for KYC and underwriting • Offer modules that can incorporate customer sentiment data |

| 5. Toolyt | • Offers field sales automation • Helps in capturing feedback during physical meetings or loan collections |

FAQs

Here are some frequently asked questions and their answers related to online review management for NBFCs and lending apps:

Ans. Reviews often act as a digital lifeline for an NBFC app’s reputation. Online app user reviews significantly influence trust, visibility, and user acquisition. In today’s financial sector, trust is a crucial part for financial service providers, such as NBFC app owners. High ratings serve as social proof, specifically, even a 1-star increase in your app’s rating can boost revenue by a huge margin. Negative reviews can severely hurt your NBFC app’s credibility, as many people may not consider downloading your app if it has a significant number of 1-star reviews.

Ans. No, you should not delete negative reviews related to high interest rates or rejected loans. Sometimes, it can feel tempting to remove a bad review from your review sites. If a bad review is making your NBFC and lending business appear negative across the web, the first thing that comes to the owners’ mind is to completely delete the review, especially from major review sites like Google. But rather than deleting the review, you can professionally respond to the feedback related to higher interest rates and rejected loans.

Ans. We suggest that you turn a 1-star review into a 5-star review by rapidly responding to it with empathy and professionalism. Through the response, you can offer a concrete solution, including a fix or a personal apology if needed. Apart from this, you can privately engage users to resolve complaints or invite them to update their review once they are satisfied with the resolution your company has provided.

Ans. There are a variety of ways you can effectively handle complaints regarding recovery agents and aggressive communication. It requires a systematic approach that starts with an immediate documentation of the harassment and escalation through formal and legal channels. The Reserve Bank of India (RBI) mandates that recovery agents must be certified and must use polite language. They should strictly follow the ‘Fair Practices Codes’.

Ans. You can automate the review management process for NBFCs and lending apps. It requires you to prioritize a ‘hybrid’ approach. You can use AI to handle high-volume and standard queries while reserving human intervention specifically for complex and negative feedback to maintain trust. Apart from this, you can implement AI to personalize responses with customer names and specific details. You can leverage AI-powered sentiment analysis to prioritize urgent issues and employ AI tools to generate tailored, humanized, and compliant responses.

Conclusion

Without properly managing your online reviews, you cannot build a strong and positive reputation for your NBFCs and lending apps. As these apps are related to loans and other critical financial services, what your existing app users are saying is extremely crucial to acquire new downloads.

When you manage your online reviews, it showcases that you truly value your customers’ opinions, and your app has become one of the most reliable resources when it comes to NBFCs and lending apps.

Initially, it may seem a daunting task, but not with an effective review management strategy plan. Our comprehensive guide will help you navigate the complex landscape of NBFC app review generation, management, and monitoring. You can explore the blog to develop a personalised review management strategy plan for your NBFCs and lending apps. If you’re still confused about how you can get started, you can seek professional assistance from a reputable online reputation management agency.